The fastest YC company to $100M and the evolving metagame for elite startups

This post has been in my backlog for a couple months. Given the viral Polymarket market predicting which crypto company ZachXBT would expose for insider trading, I decided to publish this piece because I believe people would benefit from a more informed understanding of Axiom.

The real story of how Axiom was able to achieve such growth in less than a year since launch has not been told, as they are a discreet team and do not publicize much about the team, culture, or processes behind their product.

For context, the following is a timeline of the saga:

| Monday, February 23 @ 07:57 EST | ZachXBT tweets that he is publishing an investigation on one of crypto's most profitable businesses later that week |

|---|

| Monday, February 23 @ 12:30 EST | Polymarket lists the event, allowing people to trade which crypto company ZachXBT will expose for insider trading. |

| Thursday, February 26 @ 08:41 EST | ZachXBT reveals that Broox Bauer, an Axiom employee, was one of multiple employees allegedly using internal tools to engage in insider trading. |

Developments are ongoing and this post is not meant to serve as investigative journalism. Rather, it explores how a two-person team with no prior crypto experience broke into the industry, built the fastest company to $100M in revenue in YC history, and what their trajectory reveals about the shape of elite startups going forward.

Axiom (YC W25) is a trading interface primarily targeted towards people trading long-tail tokens (polite term for memecoins) on Solana. Axiom was founded by two individuals and hit $100M in revenue in just 117 days. This is over twice as fast as the most hyped AI and financial applications such as Cursor, Lovable, and Ramp that consistently dominate headlines and mindshare.

Interestingly, one of the few public advertisements for Axiom is this campaign run by the Solana Foundation and a VC firm who isn't even on their cap table. The ads aim to legitimize crypto as a viable industry to prospective founders in San Francisco:

Axiom represents a new company archetype: one that sits at the intersection of relentless focus, monetary incentives, willingness to enter competitive markets with mediocre talent, and a third-derivative product.

In this post, I explore how Axiom became the fastest YC company to $100M in revenue and one of the highest revenue per employee companies ever.

- Background on Axiom

a. The Team Behind Axiom

b. Axiom's Business Model

c. Axiom's Revenue Numbers are Misleading

- Just Win: Inverting Consensus Advice

- Third Derivative Products

- AI Compresses the Insight-to-Execution Pipeline

Following this analysis, I provide commentary on Axiom and the shape of this company archetype moving forward.

1. Background on Axiom

The Team Behind Axiom

Axiom was started by two co-founders, Henry Zhang (ex-TikTok) and Preston Ellis (ex-DoorDash). Axiom has only raised capital from YC, and has not sold any more of the company.

Unlike other crypto teams who have historically sought to de-risk themselves by raising large seed and Series A rounds before launch, Axiom embodies the YC ethos of shipping, iterating, and talking to customers. Axiom ships and communicates frequent updates to their users via Discord and Twitter.

Axiom has since grown its engineering team in Austin to scale out its product. The majority of the core infrastructure has been built by Henry and Preston.

Axiom's Business Model

Axiom makes money by charging trading fees and selling order flow. [1] Like Robinhood and other traditional brokerages, Axiom is a frontend and does not own any of the underlying infrastructure.

Axiom currently processes $50M - $75M of daily volume. Trading fees are charged based on volume. Axiom charges 1% on every trade at execution. Depending on your account's volume, Axiom pays users back via a rebate, lowering the net effective fee. Their public cashback fee tiers range from 0.05% to 0.25%. This means that a user's net fee ranges from 0.75% to 0.95%.

For context, users trading US equities typically pay 0.05% (5 bps) or less per trade. Axiom is able to charge an order of magnitude more because memecoin traders are extremely price inelastic. Axiom users operate in an asset class with an extremely convex payout profile (users either expect assets bought on Axiom to increase in value by 10x or go to 0 within hours, sometimes minutes). Because of this dynamic, users are willing to pay high fees for a best-in-class user interface and trade execution.

By default, trades on Axiom are sent with 20% slippage (the majority of users do not change this setting). This means that the user is willing to accept a 20% worse price if it is able to be executed. If an asset has a notional value of $100, users express a willingness to accept $80 as long as they can buy or sell the asset. While slippage theoretically works both ways, users almost never receive positive slippage (receiving more than they initially anticipated). Positive slippage is typically captured and retained by a sophisticated party at some point in the supply chain.

Like Robinhood, Axiom also makes money from selling user order flow (PFOF). Axiom's order flow is extremely valuable because it is non-toxic (originates from normal retail users) and high volume. The majority of the order flow is being sold to Temporal, a Solana-native research and trading firm founded by individuals with backgrounds from Citadel and other traditional trading firms. Axiom routes order flow to Temporal, which is responsible for actually executing the order flow. Temporal abstracts the execution complexity of actually landing the transaction on-chain for developers. Running infrastructure to execute order flow is a highly competitive business in crypto with high technical, operational, and economic barriers to entry (large amounts of tokens are required to run validators).

The entities that Axiom sells order flow to are responsible for executing the order flow in the same way that Citadel is responsible for executing the order flow on Robinhood. PFOF, implemented correctly, increases user welfare, as users receive better prices. However, in the unregulated crypto arena, the little to no oversight by any regulatory committee has translated into recurring abuse of users. While Robinhood users enjoy price improvements from order flow segmentation, Axiom users often get maximally exploited by actors throughout the supply chain.

Axiom's revenue numbers are misleading

Axiom's business model of charging 1% upfront and variable rebates leads to misleading numbers. Charging someone $100 but immediately giving back $50 should not be marked as $100 of revenue.

Axiom's documentation site outlines the variable cashback tiers based on trading volume. However, this is misleading as select large and early users have non-public side-deals with Axiom that increase their cashback rate.

Many of their early users are receiving 50%+ cashback for an effective fee of much less than 0.50%. Because trading terminals like Axiom are so top-heavy (with a few users generating much of the volume and fees), Axiom's top-line $100M revenue metrics are an overestimate.

Axiom's public revenue numbers do not include additional revenue from selling order flow to Temporal. While the details of that arrangement are non-public, this is likely in the high seven-figure range depending on volume.

Because Axiom's business has many obfuscated components, it is difficult to accurately assess their top-line revenue from an outside perspective.

2. Just Win: Inverting Consensus Advice

The consensus VC view is that one should only invest in companies with structural moats, or at least in companies with a clear pathway to creating one. They believe that moats are a necessary component of great companies because they allow companies to operate as a monopoly, enabling them to extract rent via their differentiated products and services. Companies that operate in competitive markets have no structural moat and are viewed as uninvestable and low status.

Ceteris paribus, one would much rather operate a company with a structural monopoly on some product or service. However, most people do not have the technical capabilities or social capital to have a real monopoly. If a company is telling you that it operates a monopoly, they almost certainly do not.

Barring extreme outliers, the sharpest college graduates are incapable of creating a durable monopoly business. Building a monopoly business requires high context, a specific thesis, and political intelligence that requires many years of networking and life experience. This has led to many top graduates chasing empty prestigious titles and careers. No one is really working.

In this world of status-chasing and people losing the plot, actually talking to end-users has become a moat in itself. While anybody can do it, it requires interacting with people many see as below their social status. This has led to many influxes of people only wanting to build companies where they are only selling to people they can bear to interact with (B2B, typically selling to engineers at other companies), if they even talk to customers at all.

Axiom inverted this advice and consciously entered an established market, outcompeting the existing players:

- Built a company in crypto with strong engineering and product backgrounds, where the talent bar is low due to crypto's deserved reputation for scams.

- Entered the memecoin space, a sub-sector of crypto with some of the lowest talent and integrity levels across tech. Many competitors did not have traditional Silicon Valley experience and lacked the institutional knowledge of how to build applications. Furthermore, many early memecoin developers got rich from the previous wave of memecoins and checked out, leading to significant adverse selection.

- Built a frontend, a thin layer around existing infrastructure and protocols with effectively zero barriers to entry and pulls from a global talent pool.

- Entered the game late (post-Trump election in 2025) when there was sufficient market demand and existing products were already generating millions of revenue (Photon, BullX, BONKbot).

Axiom brought Silicon Valley product experience to a set of users willing to pay high fees. Much of their initial growth can be attributed to just doing the basics: focusing on a niche, talking to users, and rapid product iteration. They penetrated the few high-volume Telegram trading groups that matter, scaling via word-of-mouth and a referral program with Axiom-watermarked graphics.

3. Third Derivative Products

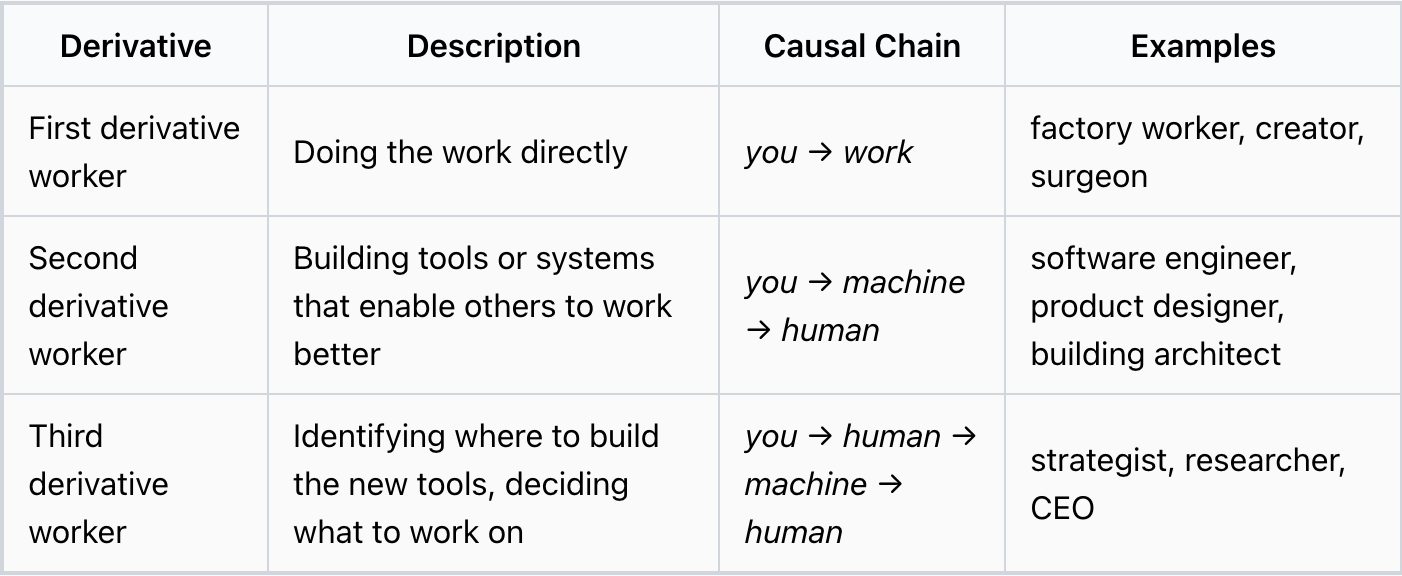

In a previous post, I outlined a theory of "derivative levels" as a way to understand why certain roles and types of work are highly compensated.