The Story of Axiom and the Future of $100M Companies Built in Under a Year

The fastest YC company to $100M and the evolving metagame for elite startups

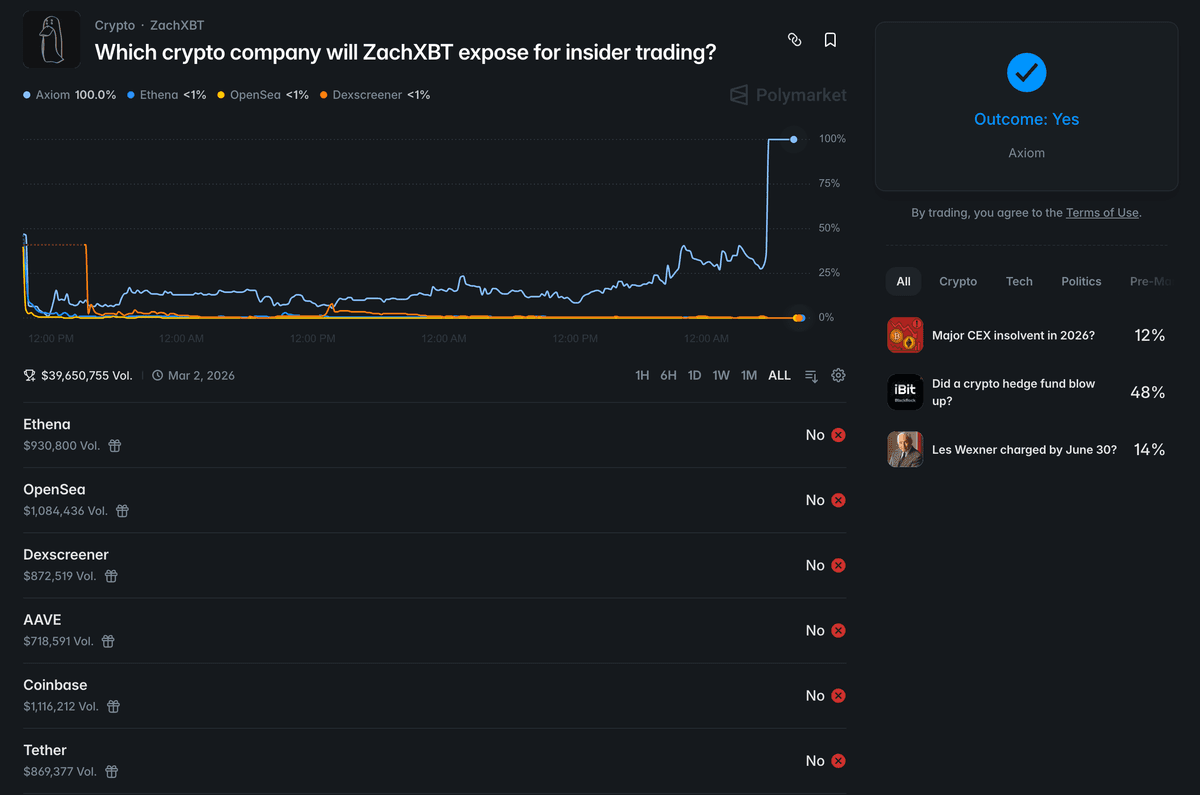

This post has been in my backlog for a couple months. Given the viral Polymarket market predicting which crypto company ZachXBT would expose for insider trading, I decided to publish this piece because I believe people would benefit from a more informed understanding of Axiom.

The real story of how Axiom was able to achieve such growth in less than a year since launch has not been told, as they are a discreet team and do not publicize much about the team, culture, or processes behind their product.

For context, the following is a timeline of the saga:

| Monday, February 23 @ 07:57 EST | ZachXBT tweets that he is publishing an investigation on one of crypto's most profitable businesses later that week |

|---|---|

| Monday, February 23 @ 12:30 EST | Polymarket lists the event, allowing people to trade which crypto company ZachXBT will expose for insider trading. |

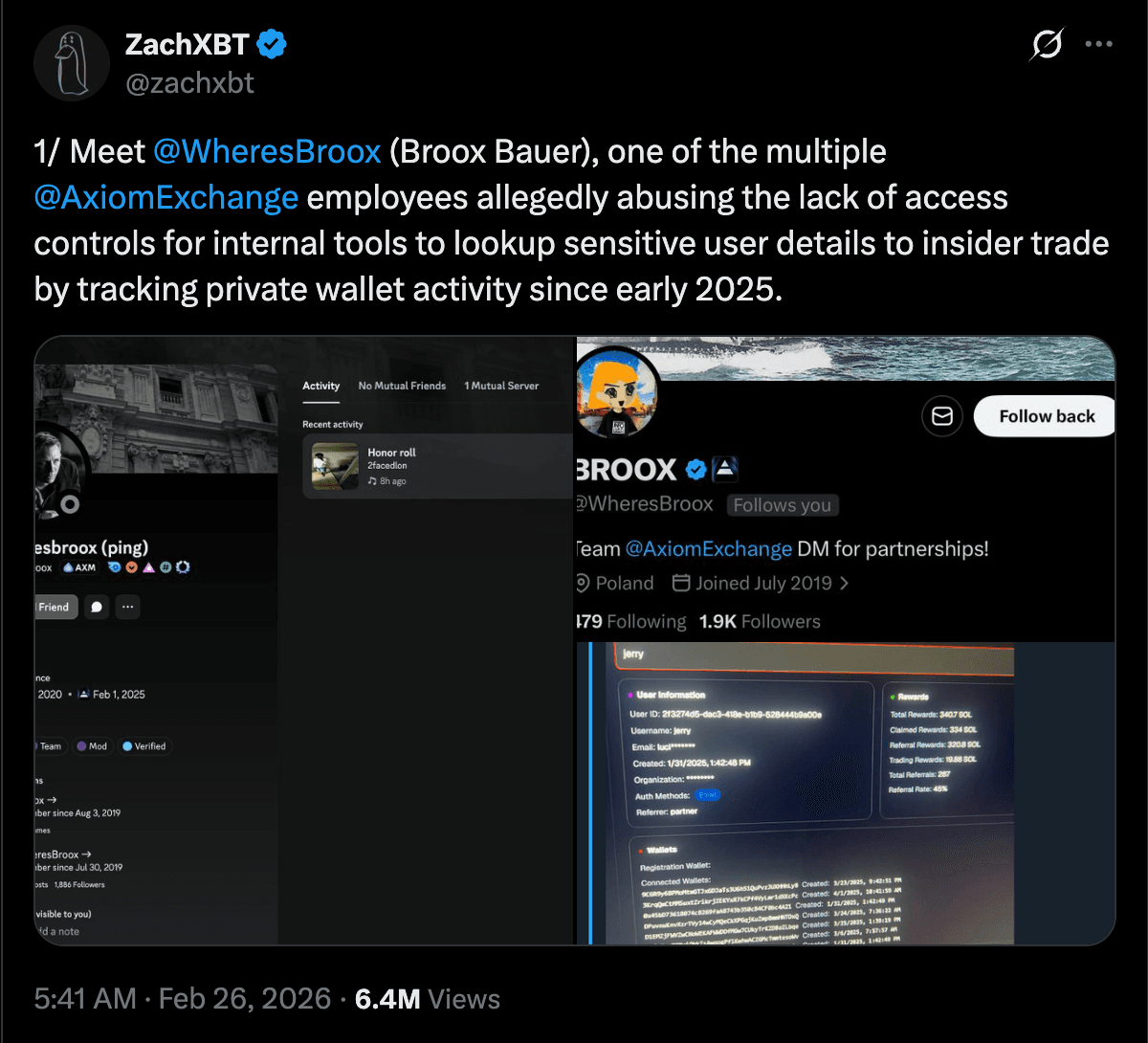

| Thursday, February 26 @ 08:41 EST | ZachXBT reveals that Broox Bauer, an Axiom employee, was one of multiple employees allegedly using internal tools to engage in insider trading. |

Developments are ongoing and this post is not meant to serve as investigative journalism. Rather, it explores how a two-person team with no prior crypto experience broke into the industry, built the fastest company to $100M in revenue in YC history, and what their trajectory reveals about the shape of elite startups going forward.

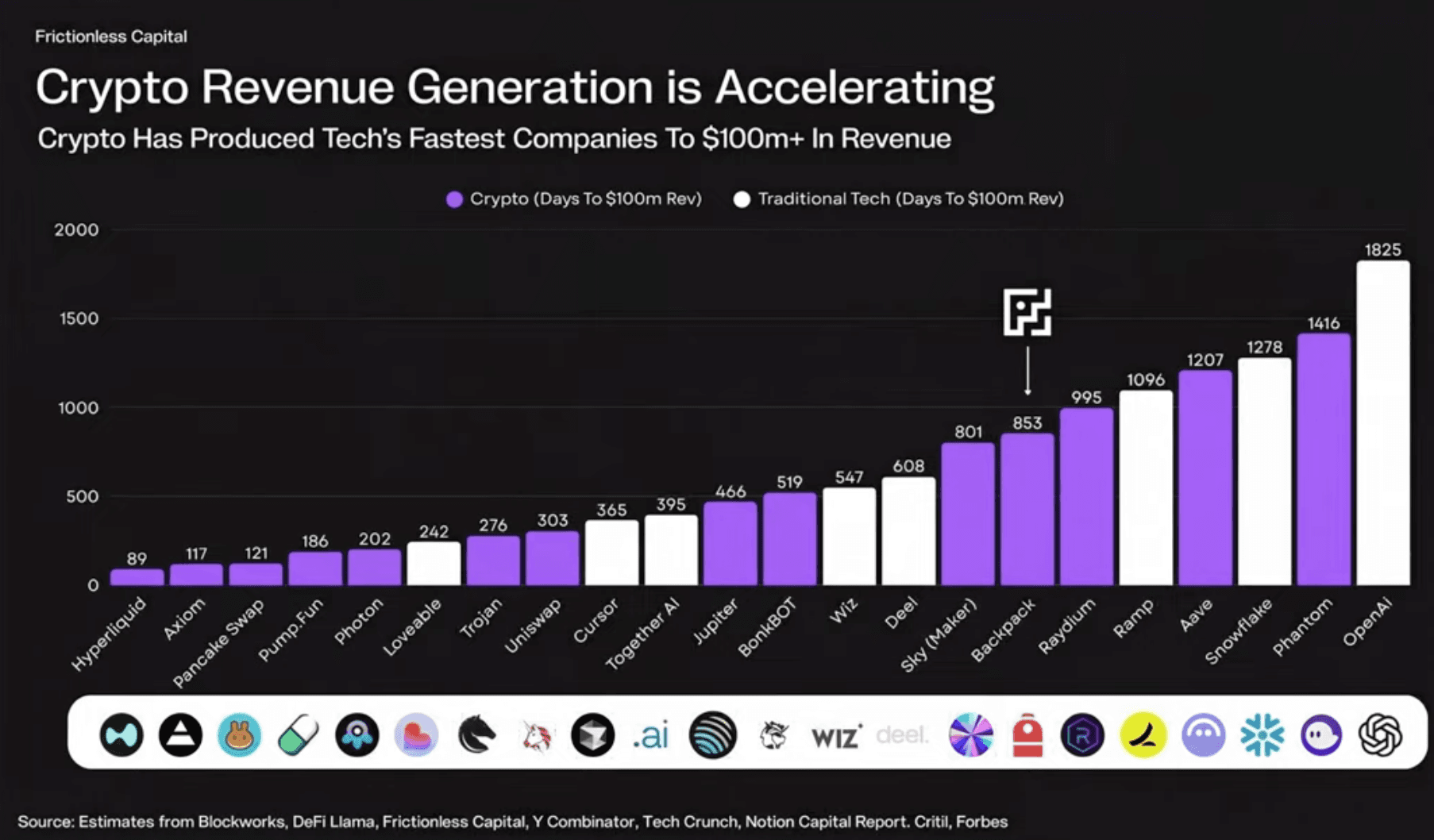

Axiom (YC W25) is a trading interface primarily targeted towards people trading long-tail tokens (polite term for memecoins) on Solana. Axiom was founded by two individuals and hit $100M in revenue in just 117 days. This is over twice as fast as the most hyped AI and financial applications such as Cursor, Lovable, and Ramp that consistently dominate headlines and mindshare.

Interestingly, one of the few public advertisements for Axiom is this campaign run by the Solana Foundation and a VC firm who isn't even on their cap table. The ads aim to legitimize crypto as a viable industry to prospective founders in San Francisco:

Axiom represents a new company archetype: one that sits at the intersection of relentless focus, monetary incentives, willingness to enter competitive markets with mediocre talent, and a third-derivative product.

In this post, I explore how Axiom became the fastest YC company to $100M in revenue and one of the highest revenue per employee companies ever.

- Background on Axiom

a. The Team Behind Axiom

b. Axiom's Business Model

c. Axiom's Revenue Numbers are Misleading - Just Win: Inverting Consensus Advice

- Third Derivative Products

- AI Compresses the Insight-to-Execution Pipeline

Following this analysis, I provide commentary on Axiom and the shape of this company archetype moving forward.

1. Background on Axiom

The Team Behind Axiom

Axiom was started by two co-founders, Henry Zhang (ex-TikTok) and Preston Ellis (ex-DoorDash). Axiom has only raised capital from YC, and has not sold any more of the company.

Unlike other crypto teams who have historically sought to de-risk themselves by raising large seed and Series A rounds before launch, Axiom embodies the YC ethos of shipping, iterating, and talking to customers. Axiom ships and communicates frequent updates to their users via Discord and Twitter.

Axiom has since grown its engineering team in Austin to scale out its product. The majority of the core infrastructure has been built by Henry and Preston.

Axiom's Business Model

Axiom makes money by charging trading fees and selling order flow. [1] Like Robinhood and other traditional brokerages, Axiom is a frontend and does not own any of the underlying infrastructure.

Axiom currently processes $50M - $75M of daily volume. Trading fees are charged based on volume. Axiom charges 1% on every trade at execution. Depending on your account's volume, Axiom pays users back via a rebate, lowering the net effective fee. Their public cashback fee tiers range from 0.05% to 0.25%. This means that a user's net fee ranges from 0.75% to 0.95%.

For context, users trading US equities typically pay 0.05% (5 bps) or less per trade. Axiom is able to charge an order of magnitude more because memecoin traders are extremely price inelastic. Axiom users operate in an asset class with an extremely convex payout profile (users either expect assets bought on Axiom to increase in value by 10x or go to 0 within hours, sometimes minutes). Because of this dynamic, users are willing to pay high fees for a best-in-class user interface and trade execution.

By default, trades on Axiom are sent with 20% slippage (the majority of users do not change this setting). This means that the user is willing to accept a 20% worse price if it is able to be executed. If an asset has a notional value of $100, users express a willingness to accept $80 as long as they can buy or sell the asset. While slippage theoretically works both ways, users almost never receive positive slippage (receiving more than they initially anticipated). Positive slippage is typically captured and retained by a sophisticated party at some point in the supply chain.

Like Robinhood, Axiom also makes money from selling user order flow (PFOF). Axiom's order flow is extremely valuable because it is non-toxic (originates from normal retail users) and high volume. The majority of the order flow is being sold to Temporal, a Solana-native research and trading firm founded by individuals with backgrounds from Citadel and other traditional trading firms. Axiom routes order flow to Temporal, which is responsible for actually executing the order flow. Temporal abstracts the execution complexity of actually landing the transaction on-chain for developers. Running infrastructure to execute order flow is a highly competitive business in crypto with high technical, operational, and economic barriers to entry (large amounts of tokens are required to run validators).

The entities that Axiom sells order flow to are responsible for executing the order flow in the same way that Citadel is responsible for executing the order flow on Robinhood. PFOF, implemented correctly, increases user welfare, as users receive better prices. However, in the unregulated crypto arena, the little to no oversight by any regulatory committee has translated into recurring abuse of users. While Robinhood users enjoy price improvements from order flow segmentation, Axiom users often get maximally exploited by actors throughout the supply chain.

Axiom's revenue numbers are misleading

Axiom's business model of charging 1% upfront and variable rebates leads to misleading numbers. Charging someone $100 but immediately giving back $50 should not be marked as $100 of revenue.

Axiom's documentation site outlines the variable cashback tiers based on trading volume. However, this is misleading as select large and early users have non-public side-deals with Axiom that increase their cashback rate.

Many of their early users are receiving 50%+ cashback for an effective fee of much less than 0.50%. Because trading terminals like Axiom are so top-heavy (with a few users generating much of the volume and fees), Axiom's top-line $100M revenue metrics are an overestimate.

Axiom's public revenue numbers do not include additional revenue from selling order flow to Temporal. While the details of that arrangement are non-public, this is likely in the high seven-figure range depending on volume.

Because Axiom's business has many obfuscated components, it is difficult to accurately assess their top-line revenue from an outside perspective.

2. Just Win: Inverting Consensus Advice

The consensus VC view is that one should only invest in companies with structural moats, or at least in companies with a clear pathway to creating one. They believe that moats are a necessary component of great companies because they allow companies to operate as a monopoly, enabling them to extract rent via their differentiated products and services. Companies that operate in competitive markets have no structural moat and are viewed as uninvestable and low status.

Ceteris paribus, one would much rather operate a company with a structural monopoly on some product or service. However, most people do not have the technical capabilities or social capital to have a real monopoly. If a company is telling you that it operates a monopoly, they almost certainly do not.

Barring extreme outliers, the sharpest college graduates are incapable of creating a durable monopoly business. Building a monopoly business requires high context, a specific thesis, and political intelligence that requires many years of networking and life experience. This has led to many top graduates chasing empty prestigious titles and careers. No one is really working.

In this world of status-chasing and people losing the plot, actually talking to end-users has become a moat in itself. While anybody can do it, it requires interacting with people many see as below their social status. This has led to many influxes of people only wanting to build companies where they are only selling to people they can bear to interact with (B2B, typically selling to engineers at other companies), if they even talk to customers at all.

Axiom inverted this advice and consciously entered an established market, outcompeting the existing players:

- Built a company in crypto with strong engineering and product backgrounds, where the talent bar is low due to crypto's deserved reputation for scams.

- Entered the memecoin space, a sub-sector of crypto with some of the lowest talent and integrity levels across tech. Many competitors did not have traditional Silicon Valley experience and lacked the institutional knowledge of how to build applications. Furthermore, many early memecoin developers got rich from the previous wave of memecoins and checked out, leading to significant adverse selection.

- Built a frontend, a thin layer around existing infrastructure and protocols with effectively zero barriers to entry and pulls from a global talent pool.

- Entered the game late (post-Trump election in 2025) when there was sufficient market demand and existing products were already generating millions of revenue (Photon, BullX, BONKbot).

Axiom brought Silicon Valley product experience to a set of users willing to pay high fees. Much of their initial growth can be attributed to just doing the basics: focusing on a niche, talking to users, and rapid product iteration. They penetrated the few high-volume Telegram trading groups that matter, scaling via word-of-mouth and a referral program with Axiom-watermarked graphics.

3. Third Derivative Products

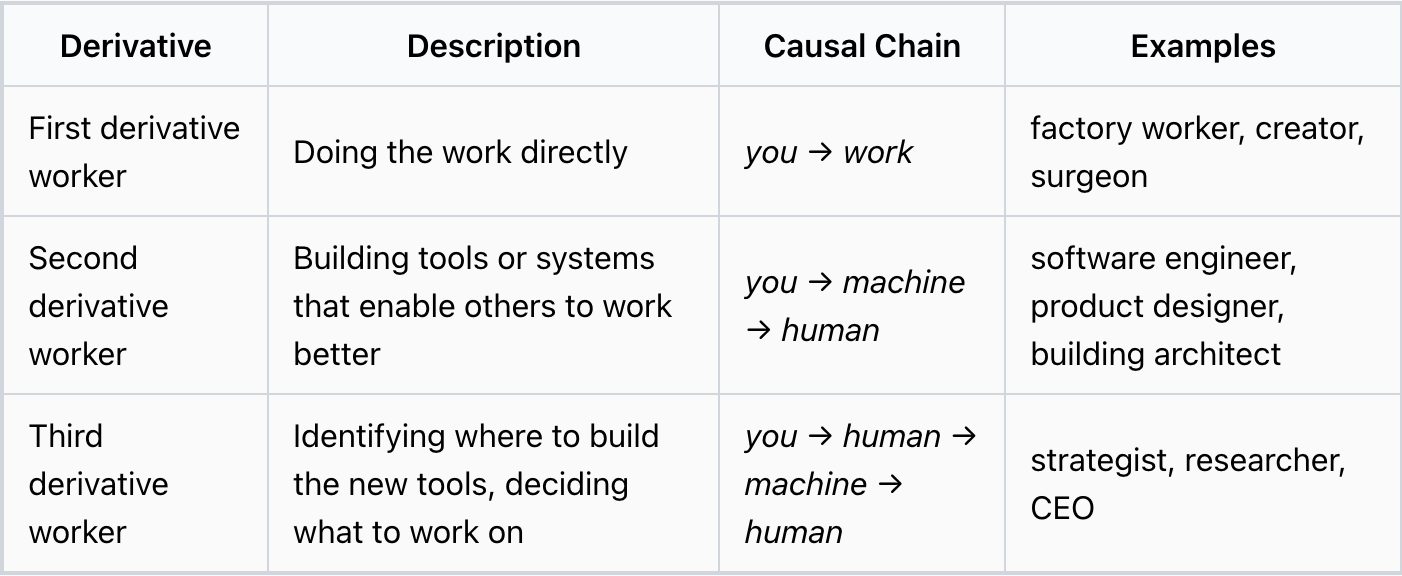

In a previous post, I outlined a theory of "derivative levels" as a way to understand why certain roles and types of work are highly compensated.

In the same way that third derivative workers identify the problems to work on and allocate human capital towards solving those problems, third derivative products enable users to identify where to build new tools and decide what to work on.

| Derivative | Description | Causal Chain | Examples |

|---|---|---|---|

| First derivative product | Does the work directly | input factors → product → world | Coca-Cola, McDonald's, Toyota |

| Second derivative product | Builds tools or systems that enable people to work better | product → human/agent → output | Cursor, Slack, Notion |

| Third derivative product | Presents what to trade/read/watch | product → human/agent → system → outcome | Axiom, Substack, TikTok, YouTube |

When you visit TikTok or YouTube, you are submitting a bid to the global video marketplace. Every time you open one of these apps, you are asking, "What should I watch right now?" The platforms fulfill their side of the trade by serving the content based on what they think you will enjoy.

When you visit Axiom, you are asking the platform, "What tokens should I trade right now?" The context is already set as memecoin traders, so even though the front page says "The Gateway to DeFi", users have context that they are there to trade high-volatility memecoins. Axiom fulfills their side of the trade by surfacing the user new tokens and allowing them to buy and trade any memecoin. Axiom users are also presented with Twitter overlays and a wallet analysis tool, which Axiom actively curates to display to the user the information they want them to see. The platform offers a unified interface that enables others to identify which tokens to trade and how to reason about the probability distribution of them making money off this token (third derivative). This is packaged in a system that also provides the means to trade the token in the same interface (second derivative).

Third derivative products are high leverage, and overwhelmingly represent the highest revenue per employee companies. Axiom, Hyperliquid, Claude, ChatGPT, Twitter, and other third derivative products enable very small numbers of people to have extreme outsized impact due to zero-marginal-cost software. Because so few companies are able to execute the product in a way that resonates culturally, they build immediate brand trust and create a self-perpetuating network effect. Many products also are able to recursively improve via proprietary model training based on user data. Once brand trust is established, these platforms become upstream of culture as people consciously and subconsciously outsource the creation of their own thoughts to these platforms.

Third derivative products tell you what to make, what to consume, and what to trade while providing unique tools and infrastructure that provide those services. They operate on the meta-level of attention and intention, providing tangible answers across domains to the question: "What should I do?"

Building a successful third derivative product is incredibly difficult. You have to provide value to the user to guide them to what they should do next in contexts you can't anticipate but have to generalize. These tools must not only be technically sound, but more importantly be epistemically correct in the context of the current culture.

4. AI Compresses the Insight-to-Execution Pipeline

While vibecoding has become commonplace among the most productive programmers today, many did not utilize AI tools to this extent in the early parts of 2025 when Axiom was initially being built. The earlier models were not as good for code generation, requiring much more engineering context to steer in an effective manner.

The founders of Axiom are extremely sharp and hardworking senior-level engineers. Their experience meant that they knew what the shape of the code should look like and where they could cut corners, enabling them to build a feature-rich application with extreme product velocity. Combined with their differentiated product insights derived through experience and tacit knowledge acquired via Silicon Valley firms and the low talent level of competitors, this meant that they were able to outcompete competitors across the board.

The combination of prior experience at traditional product-led companies (TikTok and DoorDash) and novel tooling enabled them to express their differentiated insights without lossy interpretation through other employees. Previously, founders were not able to express these insights at scale, but did not have the bandwidth to be close enough to the ground to manage all small details. This enables much better customer understanding and creates much tighter feedback loops.

Knowing What to Build and What to Optimize

Axiom is able to achieve extreme product velocity because they operate as a simple web app wrapper. Axiom avoided building complex or high-security infrastructure that would have required months of code review and auditing. Instead, they utilized third-party providers such as Turnkey, which manages user logins and wallets. The transaction landing infrastructure is handled by Temporal and actual asset transfer is handled by Solana. Axiom's edge is orchestrating existing infrastructure in a way that is engaging for end users. They knew that their moat was applying differentiated product insights to an underserved set of users.

Unlike many other teams who either naively use third-party products off the shelf or try to build everything in-house, Axiom made targeted optimizations that actually improved the end user experience. While other Turnkey applications naively use their SDKs, Axiom performs browser-specific private key optimizations. This enables them to cut latency by saving one round-trip to Turnkey's hosted infrastructure and to send transactions directly from the user more efficiently.

Dark Patterns

Axiom's product insights range from better onboarding flows for referrals to implementing select dark patterns. Dark patterns are user interface designs that are designed to trick or manipulate users to do things they didn't mean to do.

To be sure, many companies employ dark patterns and aren't strictly deceptive or bad. Common dark patterns include making it difficult to cancel subscriptions and disguised ads. The deceptiveness of these patterns exists on a spectrum from being fairly innocuous and well-accepted to straight up lying to their users.

Some of Axiom's dark patterns include:

- The cashback rebate system

- The lack of transparency around order flow management

- How they present reclaiming state rent back to the user [2]

- Affiliates and sponsorships

The inventiveness of the dark patterns implemented throughout the app is a subjective cultural judgment and is left as an exercise to the reader.

The Next Iteration of Elite, High-Growth Startups

Regardless of your opinion about crypto and the durability of Axiom as a business, Axiom is a clear harbinger of how AI is reshaping elite, high-growth startups.

I have a separate post in the pipeline about how AI changes workplace dynamics, founder incentives, and salary justifications. Across the board, Axiom illustrates many changes on the horizon:

- AI increases the value of judgment, derived via secrets and differentiated outside knowledge, as speed becomes largely commoditized.

- AI enables lower headcount and more leverage per employee, increasing the blast radius of decisions. In turn, companies will pay more in equilibrium as an insurance premium and to decrease the likelihood of spinouts.

- Axiom had some of the highest salaries for software engineers, advertising salaries well over $500k per year and covering all expenses.

- AI increases the visibility for the company to accurately assess worker productivity, increasing turnover.

- AI increases the value of social and political intelligence and intuition.

The success of Axiom has naturally legitimized trading terminals as a business, leading to much higher-caliber talent entering the space and building competitive products. The enterprise value of Axiom on February 25, 2026 likely hovered around $1-3B. As of February 26, 2026, due to the ZachXBT exposé and a multitude of other factors, their enterprise value is certainly much less and likely trending downward.

Young, immature founders lack the social intelligence and intuition to navigate the political minefield. It is clear that the 2010s and 2020s uniquely favored the one-dimensional technical founder, and that era is coming to an end. Over and over, we see this founder archetype fail to implement standard security or accounting measures and make clear hiring errors. Often, this stems from being too removed from understanding the human condition and becoming far too trusting of others. While they have been able to compensate via sheer technical prowess, they have not been able to create durable and cohesive companies that stand the test of time.

There is no single predetermined path to building a great business. Successful third derivative companies are stewarded by people with differentiated personalities and life philosophies (Sam, Dario, Elon, Jeff, etc.). Navigating the hyper-online, main-character meta is now a requirement, and many people are still not able to assess or develop the traits required to transform an early-stage elite, high-growth startup into something greater.

[1] Axiom also makes money off of staking income. Their fee profit is denominated in SOL, which they then stake on Solana to earn staking income. This is public, as they operate their own validator. This is a common setup for application teams on Solana.

[2] When a user interacts with Solana, they have to pay rent to store data on-chain. When a user closes an account (e.g. an account associated with a specific memecoin or token), they receive their money back.